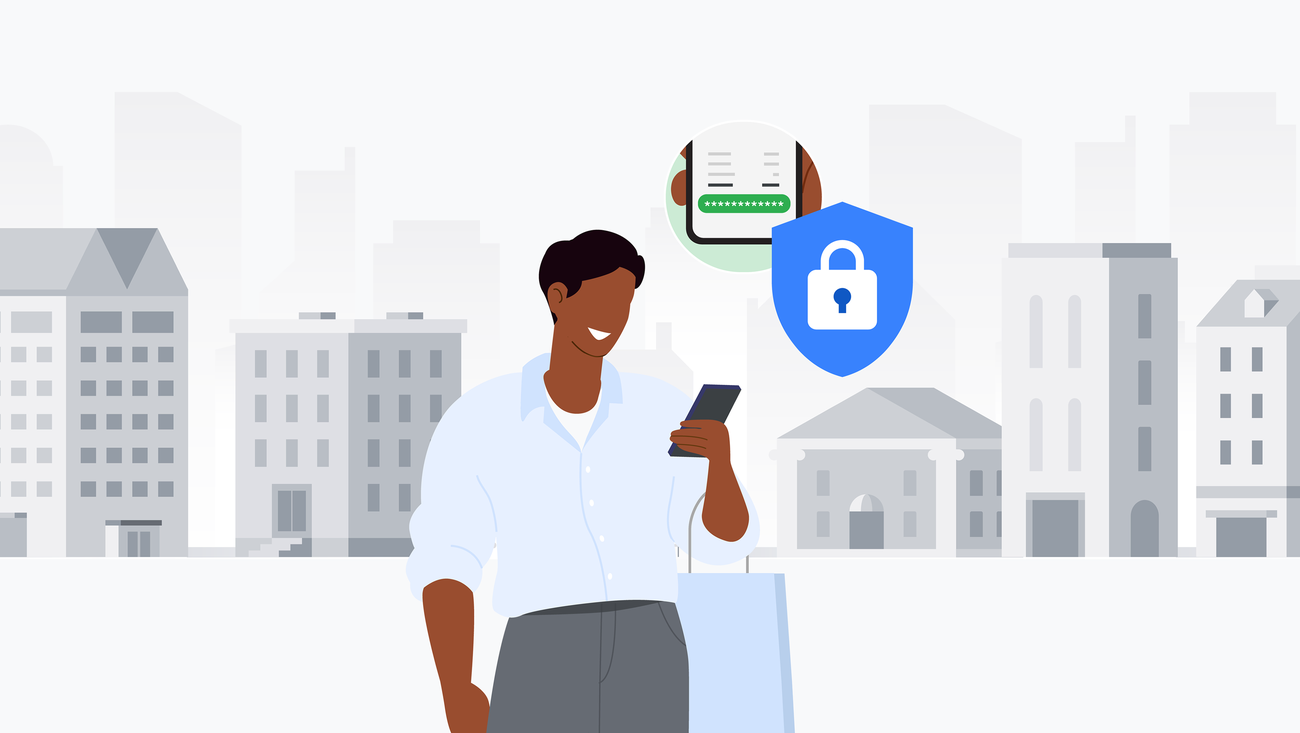

AMSTERDAM — The friction point in most online purchases is not the card number. It is the moment after you click “place order” when a site sends a one-time passcode to your phone, asks you to confirm your identity on a separate screen, or bounces you to your bank’s authentication portal before the transaction goes through. That moment is where Google has decided to plant its flag.

At Money20/20 Europe this week, the company announced a set of coordinated updates to Google Wallet and Google Pay that, taken together, represent something more significant than product features: a deliberate strategy to make identity verification and payment a single, continuous act rather than two separate hurdles at the checkout.

The headline item is geographic. Google announced it will bring digital ID passes in Google Wallet to select European Union member states this summer — the first move into EU territory after earlier launches in Brazil, India, Taiwan, Singapore, and the United Kingdom. The company did not name specific countries. What it did name was the underlying logic: that a government-recognized credential stored on a phone should be usable in the same transaction flow as a credit card, without requiring the user to carry a separate document or open a separate app.

The EU timing is not incidental. The bloc’s eIDAS 2.0 regulation, which mandates that member states offer citizens a digital identity wallet by 2026, has created both regulatory pressure and an opening for third-party platforms. Google is not building a government wallet — it is building infrastructure that governments, banks, and merchants can plug into. Whether that distinction satisfies European regulators who have historically been suspicious of large American platforms handling identity data is a question the announcement leaves unresolved.

The age verification piece is the more immediately practical piece of this. Google is working with Sparkasse, Germany’s largest banking group by customer count, to allow Sparkasse customers to confirm they meet an age requirement without disclosing their name, address, or date of birth. The technical approach relies on a selective disclosure credential: the Wallet presents a cryptographic proof that the user is above a threshold age, nothing more. P.J. Linarducci, Google’s vice president for consumer payments product management, described the goal as ensuring “companies engage with customers in age-appropriate ways while keeping sensitive user information private.”

The Sparkasse partnership is the mechanism, but the problem it is solving is wider. Age verification online has been a mess across the industry — sites ask users to upload ID documents, enter birthdates that anyone can fabricate, or click through disclaimers that no one reads. A credential-based system that pushes only what is necessary to verify eligibility is, in principle, a cleaner solution. Whether merchants outside Germany adopt it is a different matter.

On the payment side, Google Pay Direct Checkout is the feature that directly targets the one-time passcode problem. The system brings payment credentials stored in a user’s Google account directly to a retailer’s checkout page, bypassing the redirect sequences that currently interrupt European online purchases. It is available immediately for merchants using Airwallex and will extend to those using Adyen’s platform shortly after. Google says it plans to scale the capability globally with additional payment processors.

Alongside Direct Checkout, Google is rolling out what it calls Secure Payment Authentication — an updated version of the authentication flow that kicks in when European regulations require additional identity confirmation after a purchase is initiated. The company’s internal testing found the revised system reduced authentication time by 50 percent and increased conversion rates by 3 percent. The rollout will begin in the United Kingdom and Poland through Visa, Checkout.com, Autopay, and Adyen in the coming months.

The 3 percent conversion lift is the number merchants will notice. In a market where cart abandonment rates hover above 70 percent and a significant share of that abandonment happens at payment authentication screens, a measurable improvement in completion rates translates directly to revenue. That is the commercial argument Google is making to payment processors and retailers — not just that the user experience improves, but that the numbers move.

The deeper strategic logic behind all of this is the same logic that has driven Google’s payments ambitions for a decade. Google’s AI shopping push through Gemini is already trying to collapse the gap between product discovery and purchase. Identity verification and seamless checkout are the final barriers between browsing and buying. A wallet that stores your government ID, your credit card, your age credential, and your loyalty passes — and can present exactly the right piece of each at the right moment in a transaction — is not a convenience feature. It is infrastructure for the entire commerce layer of the internet.

What Google cannot control is the integration side. The digital ID expansion only matters if EU governments certify Google Wallet as an accepted presenter of their national credentials. The age verification system only spreads if more banks follow Sparkasse. Direct Checkout only reduces friction if the merchants users actually shop at adopt Airwallex or Adyen. Privacy questions around Google’s data handling in Europe remain a structural concern that no product announcement resolves.

The company is, at bottom, building a credentialing layer and betting that enough of the commerce ecosystem will choose to route through it. The technical case is solid. The business case is compelling. Whether the regulatory and adoption case holds across five or more EU jurisdictions — each with its own national digital identity program — is a question that will not be answered this summer.