NEW YORK — The number Intel’s board was staring at Monday afternoon wasn’t on any earnings slide. It was Nvidia’s closing price, up more than 6%, after CEO Jensen Huang walked onto a Taipei stage and declared that the personal computer — the device Intel dominated for three decades — had just been reinvented.

By the time U.S. markets closed on June 2, the S&P 500 had risen 0.26% to 7,599.96, the Nasdaq Composite had gained 0.42% to 27,086.81, and the Dow Jones Industrial Average had added 46.42 points to settle at 51,078.88. All three indexes reached all-time intraday highs and closed at records simultaneously — a feat they managed even as oil prices climbed and fresh reports of stalled U.S.-Iran ceasefire talks sent a warning signal that most of the market chose to ignore.

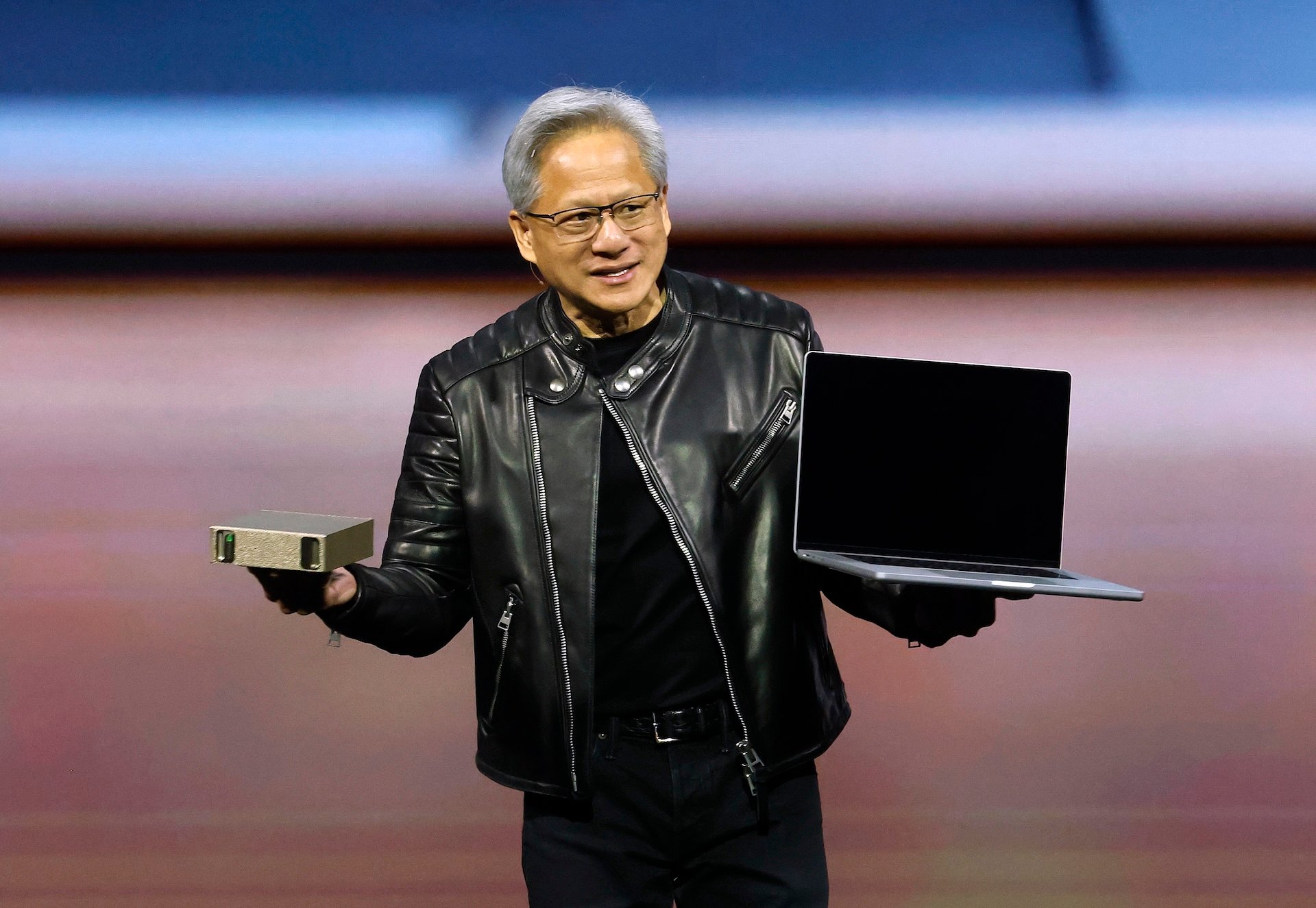

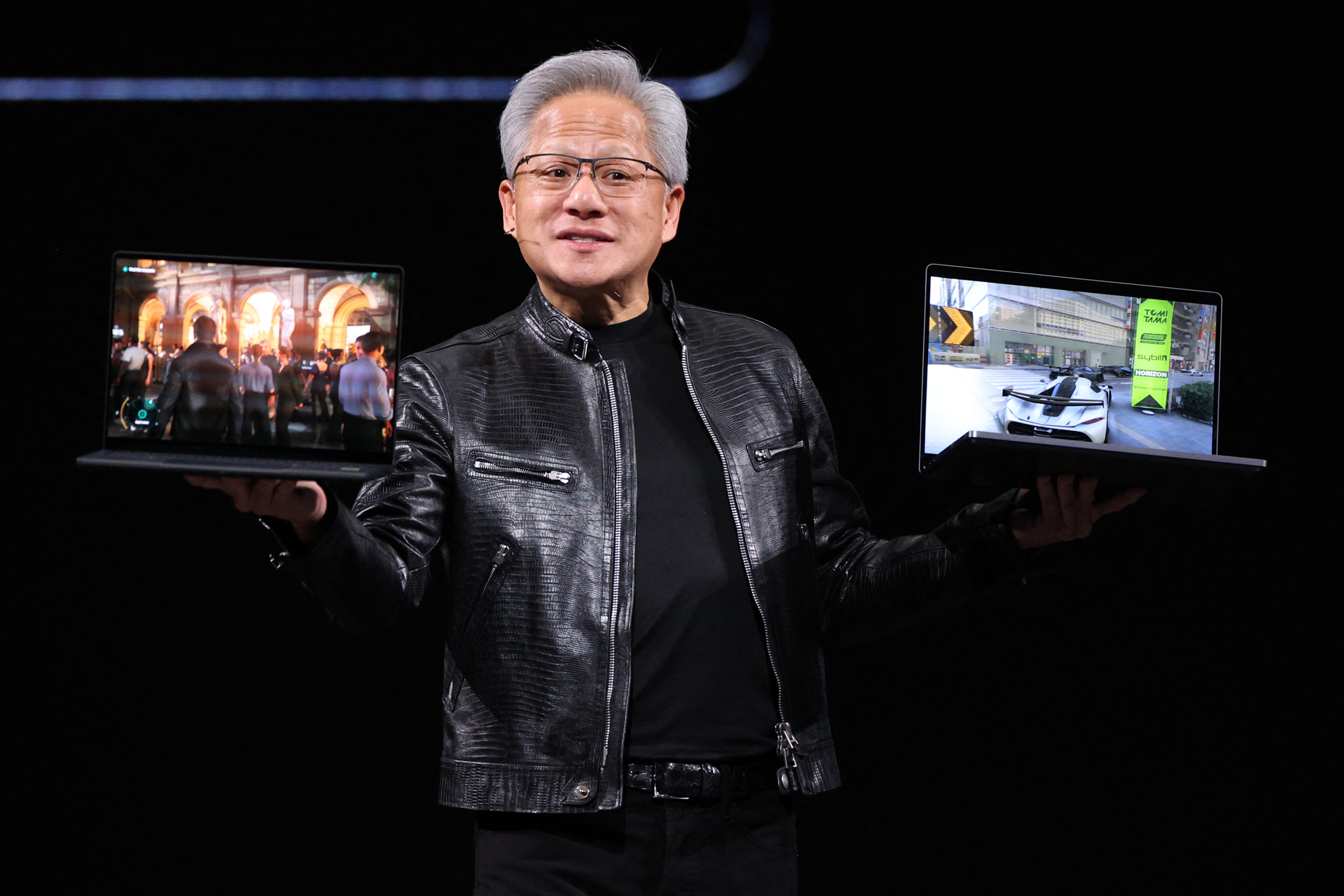

The proximate cause was hardware. At Computex 2026 in Taipei, Huang unveiled the RTX Spark Superchip — an Arm-based processor co-developed with Microsoft that places an RTX 5070-class GPU and the full CUDA software stack inside a thin Windows laptop. Dell Technologies and HP Inc., confirmed manufacturing partners, surged more than 10% and 8% respectively. Arm Holdings, whose architecture underpins the chip, gained 14.5%. Intel fell more than 4%. Qualcomm dropped 9.5%.

Huang told the Computex crowd that fall devices from Dell, HP, ASUS, Lenovo, Microsoft Surface, and MSI would make it possible for a user to simply ask the machine to do work — no apps, no clicking, no typing. “With RTX Spark and Microsoft Windows, you ask — and the PC does the work,” he said. Whether that pitch survives contact with a consumer credit card is an open question that no one in the market was entertaining on Monday.

The broader story, though, is not the chip. It’s what the chip’s effect on markets reveals about the architecture of the rally itself.

Julian Emanuel, senior managing director at Evercore ISI, published a note Sunday that put the dynamic plainly: the index’s strength and the index’s vulnerability are now the same thing. “Record concentration in handful of AI names is spurring index strength and subduing the side effects of a challenging geopolitical/consumer backdrop,” Emanuel wrote. Micron, Nvidia, and Alphabet alone accounted for more than 40% of the year-to-date revision in S&P 500 2026 earnings-per-share estimates, he said, and contributed to the strongest EPS surprises outside of recession recoveries. “Heightened index exposure to a select few names in one theme can also accentuate downside,” he added.

Emanuel has a year-end price target of 7,750 on the S&P 500, with a 30% probability assigned to a bull case of 9,000 — a scenario he ties to AI-driven productivity growth and the same structural shift that made the 1920s and 1990s such anomalous decades for markets. He also warns that a renewed escalation in the Middle East could pull the index back toward its 200-day moving average near 6,800. Monday’s session illustrated both halves of that analysis in a single afternoon.

Energy was the only other S&P 500 sector in positive territory Monday, its gain fueled by the same geopolitical uncertainty that chip stocks chose to discount. Oil prices moved higher as reports circulated that the U.S.-Iran ceasefire talks had stalled, with no fresh deal to extend or formalize a pause in hostilities. The two sectors — technology running on AI optimism, energy running on war risk — ended up pulling in the same direction, which is not a dynamic that holds indefinitely.

That tension sat beneath an otherwise buoyant session. Wall Street has spent months navigating the intersection of a war-driven commodity shock and an AI-driven earnings boom, with the latter consistently winning. First-quarter S&P 500 earnings are tracking a blended growth rate above 28% — the fastest since the fourth quarter of 2021, according to FactSet — with information technology alone posting blended growth north of 54%. That is the number the market is trading on.

Nvidia has been the load-bearing wall of that earnings story. The company reported $81.6 billion in revenue for its most recent quarter, smashing estimates, and its stock entered Monday already up sharply on the year. The RTX Spark announcement layered a new market on top of the existing AI infrastructure trade — not data centers this time, but the 150 million laptops shipped globally every year, a market that Intel has owned and that Nvidia has now formally entered. TechCrunch reported that more than 100 Windows software makers, including Adobe and Xbox, have signed on to support the new chip.

What the announcement did not settle is pricing. Nvidia confirmed that initial RTX Spark systems will target the premium segment, but no specific figures were attached to any device. The closest reference point is Nvidia’s own DGX Spark mini-computer for developers, which carries a $4,800 price tag. Whether the consumer versions will sit near that figure or come in at a level that broadens the market meaningfully remains unanswered. That gap between the ambition of the announcement and the practicalities of consumer adoption is where the trade gets complicated — and Monday’s 6% Nvidia surge did not resolve it.

Bitcoin also declined during the session, a data point Evercore noted in passing. Consumer sentiment remains depressed by energy prices and sticky inflation, with core PCE running at 3.3% year-on-year — its highest reading since 2023. None of that mattered to the headline indexes on Monday. The question Emanuel left open, and that the market has not yet had to answer, is how long that insulation holds if the geopolitical backdrop deteriorates from an annoyance into a shock.

The S&P 500 has now posted nine consecutive weeks of gains. The Nasdaq closed May up 8% for the month. All three major averages have reached records in what amounts to a near-uninterrupted advance since the April lows. The AI trade has been the engine. The engine, as Evercore’s Emanuel framed it, is now running on a very short track of names.