China’s vast smartphone market, long a bellwether for global consumer tech demand, stumbled at the start of 2026. Yet in a striking twist, Apple surged ahead, defying industry headwinds that have rattled competitors and reshaped pricing strategies across the sector.

Shipments in China declined 4% in Q1 2026, according to Counterpoint Research, as rising component costs and supply chain disruptions weighed heavily on manufacturers. The decline underscores a broader slowdown gripping the global smartphone industry, where demand is cooling even as production costs climb.

At the center of the disruption is a growing shortage of memory chips, driven in part by surging demand from artificial intelligence infrastructure. As semiconductor makers prioritize higher-margin AI applications, smartphone manufacturers are being forced to absorb higher costs or pass them on to consumers. The result has been a wave of price increases across many Android brands, dampening consumer appetite in the world’s largest smartphone market and reflecting global semiconductor market volatility.

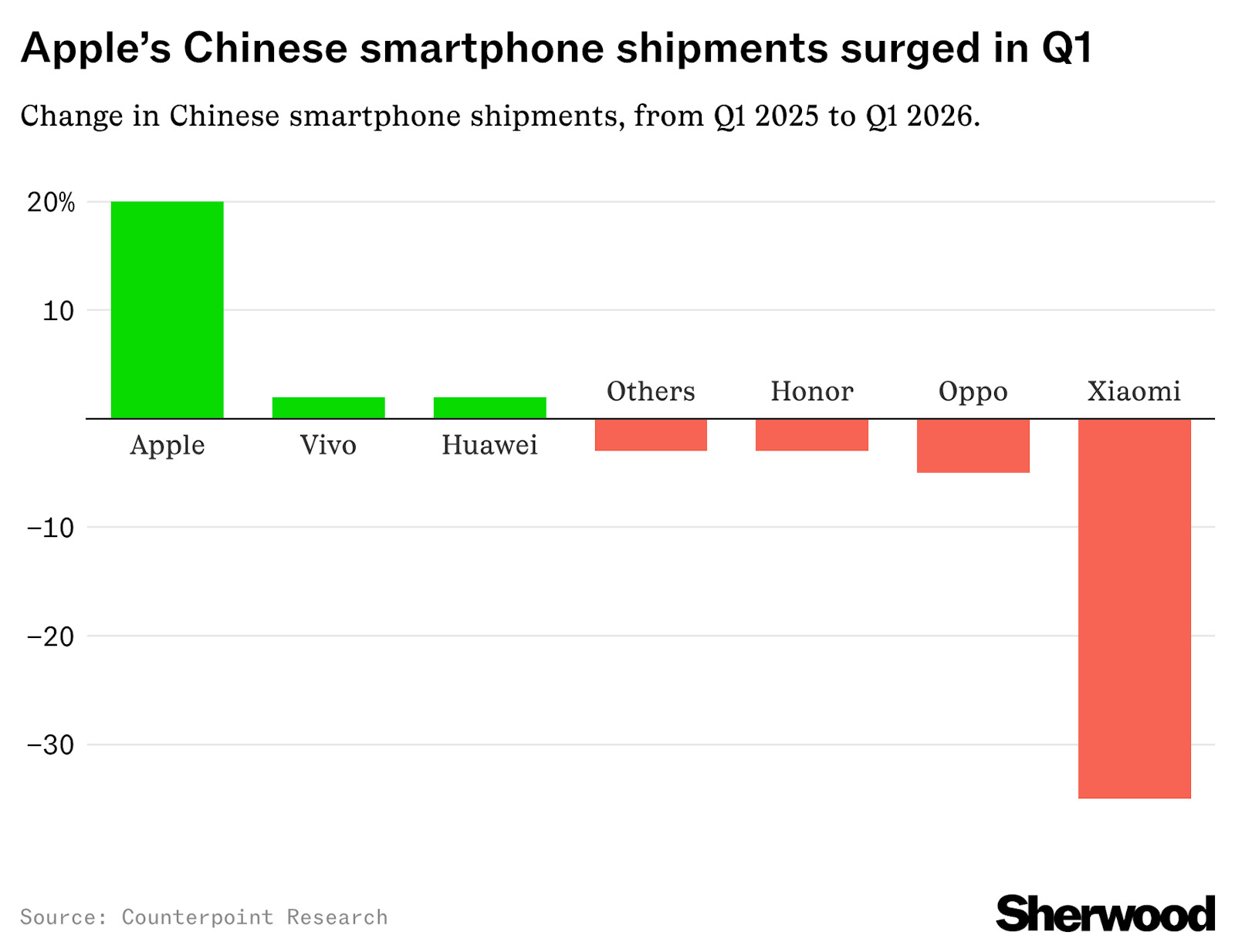

The company’s iPhone shipments in China surged 20% in China in the first quarter, the fastest growth among major vendors. While rivals struggled to maintain volumes, Apple leaned into a strategy of holding prices steady, even as input costs rose.

Analysts say that decision may be paying off.

As most rivals raise prices, Apple stands out for value, particularly in a market where consumers are increasingly prioritizing durability and long-term performance. In a market where replacement cycles are lengthening, Apple’s reputation for longevity appears to be resonating. The company’s broader roadmap, including Apple’s next big iPhone innovation, is also helping reinforce consumer confidence.

The surge also highlights a shift in consumer behavior. Premium smartphones, once considered discretionary purchases, are increasingly viewed as long-term investments. Apple’s ecosystem — spanning devices, services, and software — reinforces that perception, helping the company retain customers even as economic pressures mount.

Huawei, too, has managed to buck the broader downturn. The Chinese tech giant posted modest growth and retained the top position in market share, driven by strong demand across both high-end and budget segments. Its ability to cater to a wide range of price points has helped insulate it from the sharp declines seen by competitors.

Others have not been as fortunate.

Xiaomi, once a dominant force in China’s midrange segment, saw shipments plunge sharply, a reversal from the previous year when aggressive pricing and government subsidies boosted sales. Oppo and Honor also reported declines, while Vivo managed only marginal growth, buoyed largely by seasonal demand during the Lunar New Year.

The diverging fortunes of these companies point to a market increasingly split between premium resilience and midrange vulnerability.

Manufacturers focused on budget devices are facing a particularly difficult balancing act. Rising memory costs have squeezed margins, forcing brands to either raise prices or scale back production. In many cases, both strategies have been deployed simultaneously, leading to reduced availability of low-cost models and weakening demand among price-sensitive consumers. These pressures are compounded by rising memory chip costs impacting smartphone prices.

The challenges in China mirror a broader global trend.

Worldwide smartphone shipments are under pressure, reflecting similar dynamics of component shortages and shifting demand patterns. Broader economic uncertainty, including global market turmoil driven by Iran tensions and rising oil prices disrupting global supply chains, has added further strain to consumer spending and manufacturing costs.

Yet within this downturn, Apple’s performance suggests a different trajectory for the industry’s upper tier.

By absorbing higher costs rather than passing them on, Apple is effectively trading short-term margins for long-term market share. The company’s scale and supply chain leverage allow it to negotiate better terms with suppliers, cushioning the impact of rising component prices. Analysts note that Apple gaining market share despite industry slowdown signals a structural shift in how premium brands compete.

That strategy may prove decisive as the market continues to evolve.

With memory costs expected to remain elevated and geopolitical tensions adding further uncertainty to global supply chains, analysts anticipate continued volatility in the months ahead. Many Android manufacturers are likely to pursue additional price hikes, potentially widening the gap between premium and midrange segments.

For consumers, the implications are clear: smartphones are becoming more expensive, and the value proposition is shifting toward longevity and ecosystem integration rather than upfront affordability.

For the industry, the stakes are even higher.

China remains one of the most critical battlegrounds for smartphone makers, not only because of its size but also because of its influence on global trends. Success or failure in this market often signals broader shifts in consumer behavior worldwide.

In that context, Apple’s resurgence carries significance beyond quarterly shipment figures. It suggests that even in a contracting market, there is room for growth — provided companies can adapt to changing cost structures and evolving consumer expectations.

As the second quarter unfolds, the key question is whether Apple and Huawei can sustain their momentum — or whether the pressures weighing on the broader market will eventually catch up with even its strongest players.

One thing, however, is already clear: the rules of the smartphone industry are changing, and not all companies are keeping pace.