TOKYO — SoftBank Group Corp. was supposed to be proof that betting everything on artificial intelligence was a strategy, not a gamble. On Wednesday, the market decided to argue.

Shares of the Japanese technology conglomerate tumbled nearly 10% in Tokyo trading after Bloomberg reported that its talks with potential creditors to raise at least $6 billion from a margin loan backed by its OpenAI stake had stalled — just weeks after the company had already cut its initial $10 billion target by 40 percent. The reason lenders gave, according to people familiar with the matter who asked not to be identified, was the same one that makes the whole AI trade uncomfortable right now: no one could agree on what an unlisted startup’s equity is worth when the music stops.

That question is no longer theoretical. Across Asian markets on Wednesday, four separate pressures converged — geopolitical, monetary, technological, and corporate — and none of them resolved in investors’ favor. Japan’s Nikkei 225 fell 1.9% and the broader TOPIX shed 1.4%. South Korea’s KOSPI, already nursing the worst run among major global indices after a circuit breaker triggered for the third time this year last Monday, lost another 4.5%. Hong Kong’s Hang Seng fell 1.1%. Only India moved against the grain, up 0.4% after Reliance Industries Ltd announced an AI data center partnership with Meta Platforms Inc. — a deal that, on any other morning, would have commanded the headlines.

What makes Wednesday’s session notable is not the scale of the losses. It is the architecture. Each market fell for a different reason, which means a single policy fix — a ceasefire, a rate signal, a chip earnings beat — would not be enough to reverse the damage simultaneously.

In Japan, the problem is at the factory gate. Producer price index inflation surged 6.3% year-on-year in May, well above analyst estimates of 5.6% and sharply accelerating from April’s 5.3% reading. The Bank of Japan, which held its policy rate steady at its April meeting in a split 6-3 vote while raising its core inflation forecast to 2.8%, is now scheduled to meet next week. Deputy Governor Ryozo Himino told a parliamentary committee this month that the central bank remains committed to further rate increases, though the timing will depend on how the Middle East conflict develops. A further hike would be the fourth in the current tightening cycle, arriving while Japan’s growth forecast for fiscal 2026 has already been cut to 0.5%.

The mechanism linking the Iran war to Japan’s bond market is straightforward, even if its endpoint is not. Higher oil prices raise import costs. Higher import costs push factory-gate inflation up. Factory-gate inflation, if it persists, spills into consumer prices, and consumer prices that run hot give the Bank of Japan cover — or pressure — to raise rates it has spent three decades trying to raise. As Eastern Herald reported Tuesday, oil near $94 is testing the one assumption Wall Street had refused to question. Yields on 10-year Japanese government bonds, already at multi-decade highs, crept higher again on Wednesday.

China’s inflation picture told a different story, and the difference is the problem. Consumer prices for May came in softer than expected, pointing to continued weakness in domestic demand and household spending. Producer prices, meanwhile, surged at their fastest pace in nearly four years, driven by Iran-war supply disruptions flowing through oil and commodity markets. That divergence — factories paying more while households spend less — is a structural mismatch that monetary policy cannot easily fix. Rate cuts would stimulate demand but accelerate producer-price pass-throughs. Holding steady leaves the supply-demand gap intact. The Shanghai Composite fell 0.6% and the CSI 300 shed 1% in morning trading.

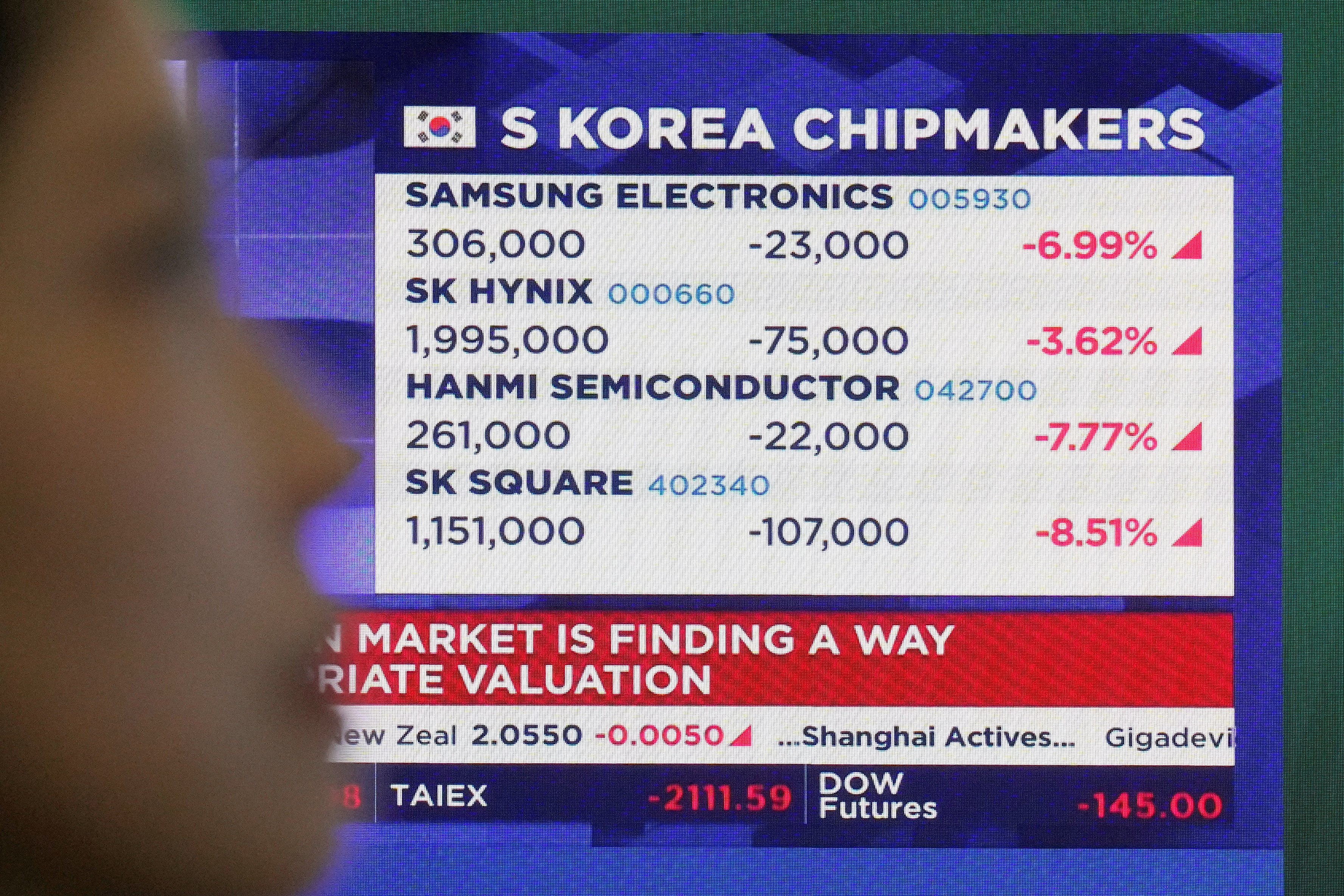

South Korea’s situation is more acute and more concentrated. The KOSPI’s collapse over the past week exposed something that Goldman Sachs, which raised its KOSPI target to 12,000 from 9,000 as recently as last month, did not fully price in: a market that becomes a single-trade index carries single-trade risk. Samsung Electronics and SK Hynix together account for roughly half the KOSPI’s market capitalization. When Broadcom reported AI chip revenue guidance for the third fiscal quarter that, at $16 billion, was about 7% below market estimates — still up more than 200% year-on-year, but not enough — the retail investors who had piled into leveraged ETFs tracking both Korean chipmakers had no natural floor. Broadcom’s $1.2 billion guidance miss erased $1.3 trillion from the chip market in the sessions that followed. The Korea Exchange has now triggered circuit breakers three times in 2026, and foreign investors have been net sellers for every session over the past month, offloading more than $10 billion of Korean equities in the week of the first halt alone.

What the SoftBank development adds to that picture is a credibility dimension. The company had, as of recent weeks, reportedly secured about $5 billion of soft commitments for the margin loan before talks went quiet. The reason cited by sources — difficulty assigning a reliable valuation to OpenAI’s unlisted equity as collateral — is not a SoftBank-specific problem. It is the same problem embedded in every fund, every leveraged position, and every earnings model that has priced AI infrastructure demand at sustained double-digit annual growth rates through the end of the decade. Nasdaq’s worst day in a year last week exposed the fault lines beneath the AI rally. If lenders who specialize in complex collateral structures cannot get comfortable with that calculation, the investor universe that can is smaller than the market has been assuming.

That uncertainty rippled through Hong Kong, where Lenovo Group fell nearly 10% after reports the personal computer maker planned to raise device prices as early as next month — a downstream consequence of Iran-war supply disruptions flowing through global electronics chains. The Hang Seng’s 1.1% decline was led by technology names, with the index’s losses compounding a week in which Wall Street’s AI stocks lost momentum as Treasury yields spiked above 4.5%.

S&P 500 futures fell 0.5% in Asian hours, with attention turning to the May consumer price index reading due Wednesday afternoon in New York. A softer print would ease pressure on long-duration AI valuations and give markets in Seoul a reason to stabilize. A number that comes in hot — as Japan’s just did — would do the opposite. Whether any single data point is enough to settle four separate arguments at once is a question the CPI alone cannot answer.