LONDON – For the buyer who completed on a terraced house in Leeds just weeks before May’s figures landed, the timing was brutal. The property, bought at the April average, is now part of a market that has reversed course – the first time in 2026 that British house prices have fallen on a monthly basis.

Nationwide Building Society reported on Monday that the average UK house price slipped 0.6 percent in May to £278,024, down from £278,880 in April. Annual growth decelerated sharply, dropping to 1.7 percent from 3.0 percent the month before. The data, which accounts for seasonal effects, marks the first month-on-month decline this year and the weakest annual pace since the autumn.

The proximate cause is not domestic. It is the war. When fighting escalated across the Middle East in February, energy markets reacted violently. Gas prices surged. Swap rates – the benchmarks that underpin fixed-rate mortgage pricing – climbed in tandem, reversing the steady decline that had been improving affordability throughout late 2024 and early 2025. Buyers who had been edging back to the market quietly reconsidered.

“Given the uncertainty caused by developments in the Middle East and the subsequent rise in energy prices and market interest rates, some loss of momentum was to be expected,” Robert Gardner, Nationwide’s chief economist, said in a statement. Consumer confidence, he noted, had fallen to its lowest level since late 2023 in April, measured by GfK’s headline index, with only a marginal recovery in May.

What Gardner did not say – but the data implies – is that the housing market had been making a genuine recovery before the conflict. Annual growth had accelerated to 2.2 percent in March and 3.0 percent in April, the fastest pace in months. The UK economy grew a solid 0.6 percent in the first quarter. Employment was holding. The trajectory was, by British housing market standards, quietly encouraging. None of that insulates the market when 90 percent of mortgage holders are on fixed-rate products tied to benchmarks that respond, almost immediately, to geopolitical shocks.

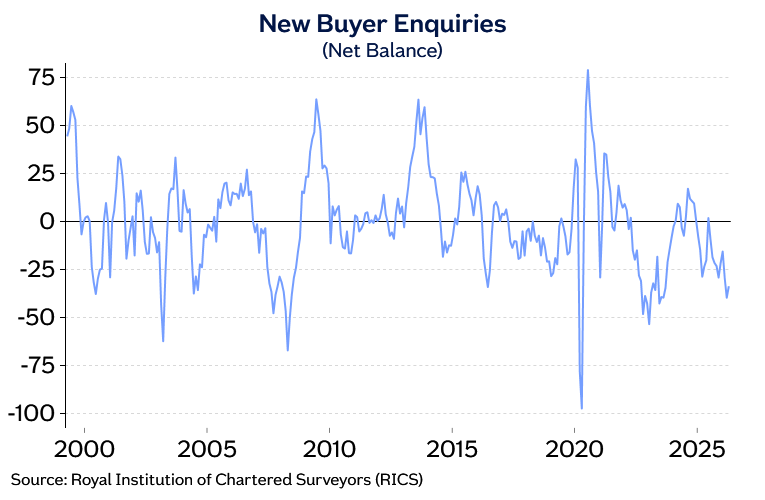

The Royal Institution of Chartered Surveyors registered a sharp fall in new buyer enquiries in March, pushing its index to the weakest reading since 2023. April offered no improvement. Sellers, caught between ambition and reality, are discovering that over-priced homes are simply not selling. “Focused, price-sensitive buyers are negotiating hard,” said Jason Tebb, president of property platform OnTheMarket, while acknowledging the market continues to function – just at a lower temperature.

Savills, the property consultancy, was more direct. Last week it downgraded its 2026 forecast for a third time, now anticipating a 2 percent fall in average prices across the year – a steeper reversal than any seen since the financial crisis. The firm said the conflict in Iran and the resultant rise in mortgage rates had fundamentally changed the outlook for the housing market. Much of the downgrade traces directly to the surge in swap rates that followed the outbreak of hostilities in February.

The precise damage done to affordability is harder to pin down. Nationwide’s Gardner is careful to note that swap rates, though elevated, remain well below the peaks of 2023 and are broadly in line with 2024 levels – implying the reversal of earlier affordability gains is partial, not total. That qualification matters. It means the market is not replicating the acute stress of the post-Truss period. But it is also not the market of early 2025, when rate cuts were expected and first-time buyer activity had risen 18 percent year on year.

Household finances, Gardner argued, provide a meaningful floor. Total household debt relative to income sits at its lowest in roughly two decades. Savings accumulated during the pandemic years have not been fully drawn down, though Gardner acknowledged they are not evenly distributed. The question is whether those buffers are sufficient if the war, and the energy shock it has produced, extends through the summer and into the autumn – a scenario that Nationwide’s own statement leaves conspicuously open.

Britain’s energy bills are already reflecting the new pricing environment. The Ofgem price cap, set ahead of the conflict’s full impact on wholesale gas, is expected to rise further this summer as UK energy costs climb on the back of the Iran war gas shock. For households managing mortgage payments alongside rising utility bills, the effective squeeze is compounding in ways the headline price figure does not fully capture.

There is a further dimension that none of the major forecasters are yet modelling with any precision: how long. Nationwide’s Gardner allows that if the shock passes relatively quickly and energy prices normalise, any near-term softening should prove short-lived. That conditional carries considerable weight. A ceasefire, or even sustained de-escalation, could reverse the swap rate trajectory fast enough to limit the damage to a single soft quarter. Prolonged conflict would likely mean something worse.

The Bank of England is watching the same data. Its rate-setting committee faces a version of the same dilemma that confronted central banks during the 2022 energy shock: a supply-side inflation push that rate hikes cannot resolve, but also cannot be ignored if it feeds into wage expectations. Markets have been pricing in further increases; Andrew Bailey signalled last week that a hike may not be necessary. The resolution of that tension will have as much bearing on house prices as anything happening in estate agent windows. As City AM reported, the Bank of England’s governor suggested an interest rate hike may not be required – a reading that, if sustained, could limit the mortgage market damage.

Meanwhile, broader pressure on British borrowing costs has rattled financial markets since the spring, adding another layer of uncertainty to the rate outlook. Whether May turns out to be a single-month blip or the opening of a sustained decline is the question no index, forecast, or central bank statement can yet answer. The market is waiting on a war to end.