SEOUL – SK Hynix raised $28 billion on Thursday, pricing its American depositary receipts at the top of their indicated range and producing what ranks as the second-largest share sale in global history, eclipsing the Alibaba listing of 2014 that had stood for more than a decade as Wall Street’s benchmark for offshore ambition.

The ADRs, listed under the ticker SKHY, began trading Friday on the Nasdaq. Alibaba’s listing had raised $25 billion; SK Hynix surpassed it by $3 billion, falling short only of SpaceX’s recent flotation in the all-time rankings. The original target for the SK Hynix offering was $29.6 billion, reduced after the company’s Seoul-listed shares fell in the weeks before pricing.

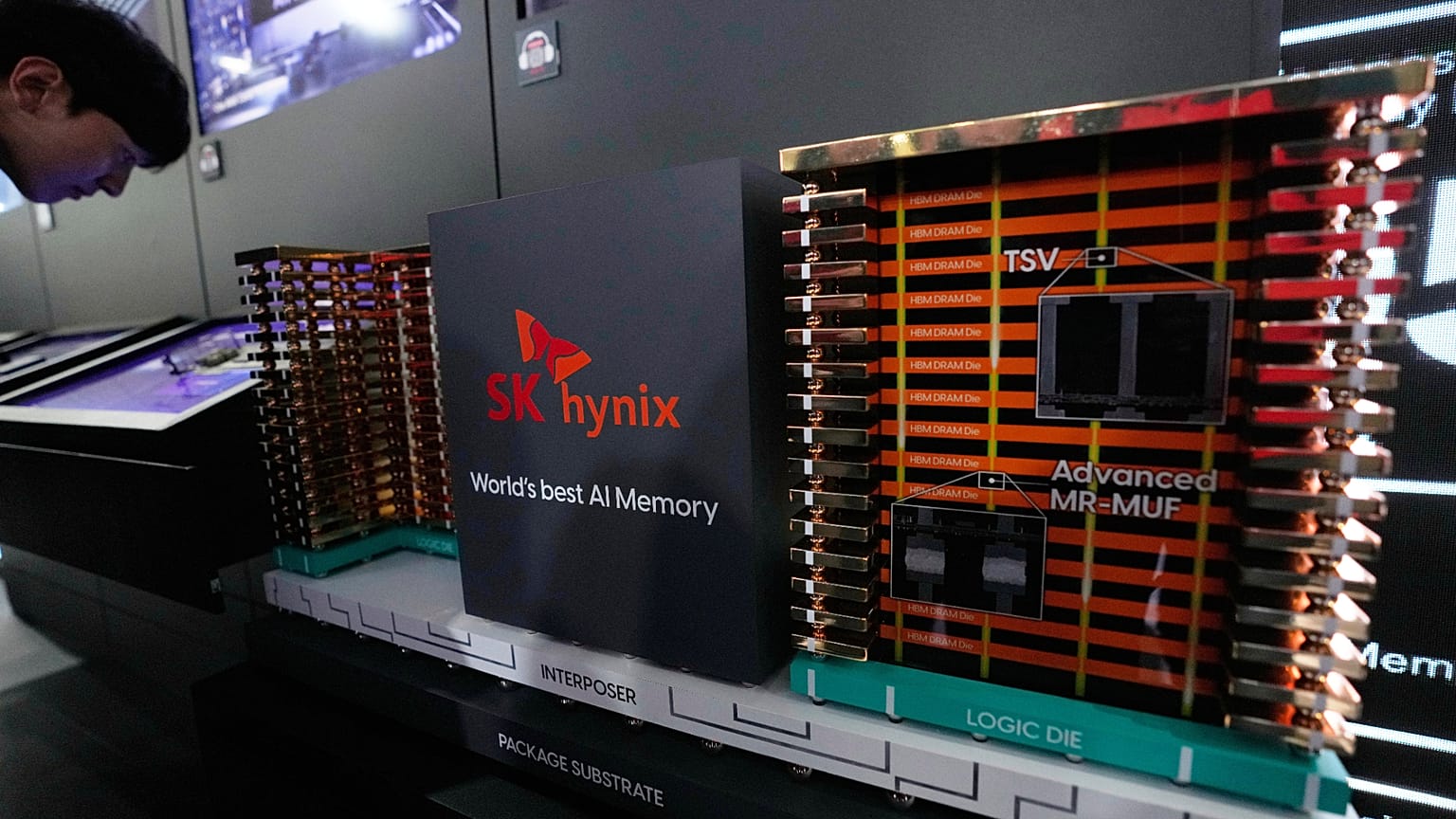

What SK Hynix was selling was more specific than most offerings at this scale. The company controls approximately 60 percent of the global market for high-bandwidth memory, the dense, power-efficient chip architecture that sits inside every major artificial intelligence accelerator in use today. Without HBM, the inference workloads that power ChatGPT, Gemini, and Anthropic’s Claude cannot run at commercial scale. Investors buying SKHY are not merely purchasing equity in a South Korean manufacturer; they are taking a stake in the component the AI industry cannot readily replace, Euronews reported.

The company’s financial position underscores the advantage. Q1 2026 revenue exceeded 50 trillion won (€29 billion), with operating margins above 70 percent, a figure more commonly associated with software platforms than chip fabrication facilities. SK Hynix’s total market valuation now exceeds $1 trillion.

Cornerstone investors anchored the offering before pricing. Baillie Gifford and Coatue Management funds collectively signaled interest in up to $7 billion of stock, providing institutional support that allowed the company to price at the top of its range despite the broader semiconductor market’s June selloff. When a global AI stock rout froze South Korea’s Kospi exchange in June, SK Hynix’s Seoul-listed shares fell more than 12 percent in a single session. That the Nasdaq listing proceeded and priced at the top signals management’s judgment that the rout was a correction, not a directional shift in the AI investment thesis.

Proceeds from the offering are earmarked for fabrication plant expansion, primarily at the Yongin cluster in South Korea, and for the company’s first US packaging facility in Indiana. The Indiana facility signals an effort to meet domestic production requirements embedded in US government AI procurement policy and to reduce logistics friction for American hyperscaler customers who prefer suppliers with a US footprint.

The choice of Nasdaq over the Seoul Stock Exchange, where SK Hynix is already listed, reflects the location of its customer base. NVIDIA, whose data center revenue exceeded $39 billion in its most recent quarter, depends on SK Hynix HBM for every GPU it ships into AI infrastructure. Alphabet, Meta, Microsoft, and Amazon are collectively committing hundreds of billions to AI data center buildout. Having SKHY on Nasdaq places SK Hynix’s equity into the same institutional portfolios that hold the companies running on its chips.

Structurally, each ADR represents one-tenth of a Seoul-listed ordinary share, allowing dollar-denominated investor access without restructuring the company’s domestic ownership. The ADR float represents a fraction of total outstanding shares, keeping existing Korean institutional shareholders largely intact while drawing American capital at scale.

The HBM supply picture is what makes the listing’s timing legible. SK Hynix holds NVIDIA supply agreements at volumes Samsung Electronics cannot currently match, as Samsung has fallen behind on HBM yield rates. Micron Technology is investing to establish itself as a third credible supplier but remains behind both Korean manufacturers in volume. Previous coverage of SK Hynix’s listing plans had noted a target as high as $29.6 billion; the $28 billion final figure still rewrote the foreign-firm record by more than $2 billion over Alibaba.

NVIDIA’s next-generation Rubin architecture requires higher HBM volumes per unit than the current Blackwell generation. Even flat aggregate AI infrastructure spending translates into higher HBM unit demand for the leading supplier, because each new GPU generation is more memory-intensive than the last.

What the Nasdaq debut does not resolve is how long the supply advantage holds. Samsung has publicly committed to HBM investment that would narrow the gap if yield rates improve. The June AI market rout showed that external factors can compress semiconductor multiples rapidly regardless of underlying demand. The $28 billion raise gives SK Hynix resources to extend its fabrication lead. Whether that lead remains intact by the time the Indiana facility opens, and whether hyperscalers sustain the AI spending levels that make HBM indispensable, are questions the listing sets in motion without answering.