TOKYO — Japanese companies increased their capital expenditures by 2.9 percent in the third quarter of 2025 compared to the previous year, a slowdown from the robust 5.1 percent expansion in the prior period, yet a figure that underscores resilient domestic demand even as global trade tensions mount. The data, released Monday by the Ministry of Finance, exceeded economists’ modest expectations of 1.8 percent growth and offers a counterpoint to recent gloomy headlines about Japan’s contracting economy, where gross domestic product shrank 0.5 percent quarter-on-quarter in preliminary figures.

This deceleration in business investment, a key driver of Japan’s post-pandemic recovery, reflects a bifurcated landscape. Manufacturing sectors, battered by anticipated US tariffs under President Donald Trump’s reelection, pulled back sharply, while non-manufacturing industries surged ahead, fueled by artificial intelligence investments and steady consumer spending. Corporate pretax profits, meanwhile, rocketed nearly 20 percent in the same period, highlighting a paradox: firms are awash in cash but cautious about deploying it amid geopolitical uncertainties.

The capital expenditure figures, covering July through September, paint a picture of an economy adapting rather than crumbling. Private nonresidential investment rose to 15.24 trillion yen ($100 billion), up from 14.81 trillion yen a year earlier, with equipment spending jumping 4.7 percent and structures up 0.3 percent. Analysts point to this as evidence that Japanese businesses, long criticized for hoarding cash, are recommitting to growth at home. “Despite external headwinds, domestic demand remains the bedrock,” said Hiroshi Nishiura, chief economist at Nippon Life Insurance, in a note to clients. The resilience is particularly notable given Japan’s Q3 GDP contraction, attributed partly to weaker exports and inventory adjustments.

At the heart of this story lies the shadow of American protectionism. Since Trump’s inauguration in January 2025, threats of 25 percent tariffs on Japanese autos and electronics have prompted manufacturers to trim investment plans. Toyota Motor Corp. and other automakers, facing potential duties on vehicles shipped to the US, reported scaled-back capital spending in surveys by the Development Bank of Japan. Semiconductor equipment makers, however, bucked the trend, pouring funds into AI infrastructure as global demand for chips explodes. This shift mirrors a broader reorientation: Japanese firms are pivoting from export reliance toward domestic and Asian markets, bolstering supply chain resilience.

Corporate profits provide the financial backstop. July-September earnings before tax climbed 19.8 percent year-on-year to a record 28.5 trillion yen, driven by tech giants like SoftBank Group and AI-related ventures. Yet profitability masks investment hesitancy. A Bank of Japan quarterly tankan survey earlier this month revealed large manufacturers planning just 7.8 percent capex growth for fiscal 2025, down from prior forecasts, as tariff fears dampen overseas expansion Smaller firms, less exposed to exports, showed more optimism, with non-manufacturers targeting 10.2 percent increases.

Tariff Turbulence Reshapes Investment Priorities

The US tariff regime has become the defining external force on Japan’s economy. President Trump’s “America First” policies, including blanket duties on imports from Japan, China, and Mexico, have forced corporate Japan to recalibrate. Automakers, which account for nearly a quarter of Japan’s exports to the US, face the brunt: Toyota alone could see $10 billion in annual costs if full tariffs materialize. In response, companies are accelerating “China-plus-one” strategies, diversifying production to Southeast Asia and bolstering domestic automation.

This caution is evident in sector breakdowns. Manufacturing capex grew a meager 0.5 percent, dragged by autos and machinery, while non-manufacturing leaped 4.8 percent, led by services, retail, and tech. Real estate investment, a perennial bright spot, contributed solidly, with office and logistics developments in Tokyo and Osaka absorbing capital amid e-commerce booms. “We’re seeing a flight to quality domestic assets,” noted Kazuto Oku, senior strategist at Nomura Securities. Such trends align with the Governor Kazuo Ueda’s long-standing push for wage growth and investment to escape deflation’s grip.

Broader economic context amplifies the capex data’s significance. Japan’s Q3 GDP fell 0.5 percent from the prior quarter and 1.8 percent year-on-year, worse than expected, as consumption softened and exports stagnated. Inflation, meanwhile, hovers near the BOJ’s 2 percent target, supporting gradual rate hikes.

AI Boom and Profit Surge Fuel Optimism

Amid the gloom, technological tailwinds shine brightly. Japanese firms’ embrace of generative AI has supercharged profits and selective investments. SoftBank’s Vision Fund poured billions into AI startups, while domestic players like Fujitsu and NEC ramped up data center builds. This sector’s vigor offset manufacturing weakness, with information and communications capex up over 10 percent.

Profit growth was widespread: manufacturing earnings rose 15 percent, non-manufacturing 22 percent. Energy firms benefited from stable oil prices, while pharmaceuticals expanded R&D amid global health demands post-COVID. Yet, executives remain prudent. A Reuters poll of 100 firms found 60 percent citing tariffs as the top risk, ahead of yen volatility or domestic slowdowns.

The yen’s 10 percent depreciation this year has cushioned exporters but inflated import costs, squeezing margins in non-tradables. Still, household spending held firm, up 1.2 percent nominally, supporting the domestic demand narrative.

Policy Response and Fiscal Year Outlook

Policymakers are watching closely. The BOJ, having raised rates to 0.5 percent in October, signals patience on further hikes until tariff impacts clarify. Prime Minister Shigeru Ishiba’s cabinet, facing upper house elections next summer, touts capex strength as proof of “Abenomics 2.0” continuity, structural reforms to boost productivity.

Fiscal 2025 projections hinge on capex momentum. Trading Economics forecasts full-year growth at 3.2 percent, but tariff escalation could shave 0.5 points off GDP. The Development Bank of Japan’s August survey showed planned capex up 8.1 percent for the year, though recent downward revisions temper enthusiasm.

Global parallels abound. Like Germany, Japan grapples with export dependence amid US protectionism. Unlike China, its democratic alliances offer negotiation leverage, ongoing US-Japan talks aim to exempt key sectors.

Implications for Global Markets

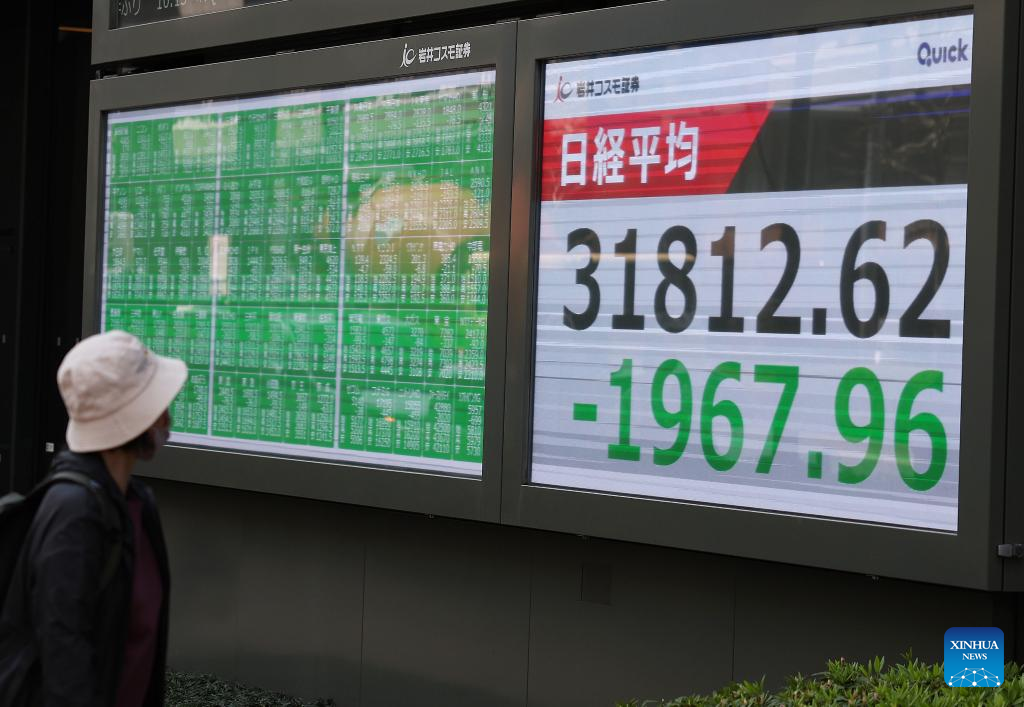

For investors, the mixed signals demand nuance. The Nikkei 225 dipped 0.3 percent Monday on GDP worries but rebounded on capex beats, reflecting market faith in corporate balance sheets. Bond yields ticked up, pricing in steady BOJ normalization.

Longer term, Japan’s capex resilience signals a maturing economy less beholden to bubbles. Demographic headwinds, a shrinking workforce, make productivity investments imperative. AI and automation offer paths forward, but tariffs test resolve.

As winter sets in, Tokyo’s salarymen hustle through salarymen districts, embodying quiet determination. Japan’s economy, like its people, bends but rarely breaks. The 2.9 percent capex rise may lack fireworks, but in an age of shocks, steadiness is strength.