BEIJING – When the South Korean market research firm SNE Research released its first-quarter battery figures in May, the headline share number – 71.4 percent of all electric vehicle batteries installed globally, supplied by Chinese companies – landed with the quiet force of a settled argument. Less than three years ago that figure stood at 60 percent. The arithmetic of the intervening period is not really about market dynamics; it is about structural capture of the most consequential component in the energy transition.

Total global EV battery usage reached 244.6 gigawatt-hours in January through March 2026, up 9.1 percent from the same period a year earlier, according to SNE Research data published by CnEVPost. Chinese producers accounted for every tenth of a percentage point of market share gained over the prior year and a half. The only question anyone in Seoul, Tokyo, or Brussels is asking is whether there is a point at which that trend reverses – and the first quarter gave them little reason for confidence.

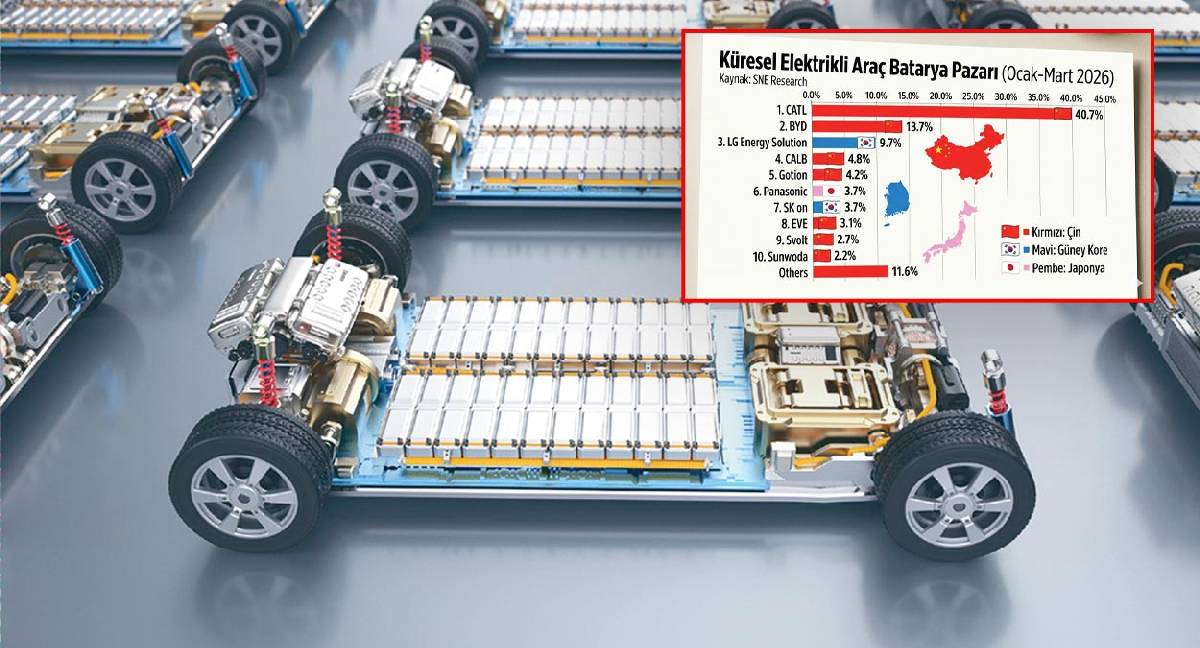

CATL, the Ningde-based company that supplies Tesla, BMW, Volkswagen, and nearly every major Chinese automaker, installed 99.5 GWh of batteries during the quarter – a 15.2 percent increase year-on-year from 86.4 GWh – and held 40.7 percent of the global market on its own. That is not a dominant position in the conventional sense; it is something closer to structural monopoly of the supply chain for the world’s fastest-growing vehicle technology. The International Energy Agency’s Global EV Outlook 2026 noted that CATL recorded operating margins of 18 percent in 2025, in a year when several of its South Korean competitors reported recurring operating losses.

BYD, the second-ranked Chinese producer, had a more complicated quarter. Its battery installations fell 8.0 percent to 33.5 GWh compared with 36.4 GWh a year earlier, and its global share slipped to 13.7 percent from 16.2 percent. SNE Research attributed the decline primarily to softer sales of BYD-branded vehicles inside China rather than any competitive setback; the company simultaneously expanded deliveries to newer clients including Xiaomi. Together, CATL and BYD accounted for 54.4 percent of every EV battery installed anywhere in the world during the first three months of this year – a combined share that would be called a duopoly in any other industry and is increasingly treated as an infrastructure dependency in this one.

The rest of the top ten underscores how thoroughly the field has been reorganized. China’s CALB ranked fourth with 4.8 percent of the market, growing 31.7 percent year-on-year. Gotion High-tech held fifth with 4.2 percent. EVE, SVOLT, and Sunwoda rounded out the Chinese contingent. Japan’s Panasonic – historically Tesla’s primary battery partner in North America – placed sixth with 3.7 percent, a position it is struggling to hold after postponing full operations at its new Kansas plant due to slowing Tesla demand. The three South Korean producers that once defined the global battery industry outside China – LG Energy Solution, SK On, and Samsung SDI – combined for 15.0 percent of the market, a decline of 2.1 percentage points from a year earlier.

LG Energy Solution, which led the non-Chinese world for much of the last decade, held 9.7 percent globally with 23.7 GWh of installations, a modest 6.6 percent growth rate. But growth at LG masks the pressure below: SK On cut roughly 1,000 jobs at its Georgia plant in early 2026 – approximately 40 percent of the facility’s workforce – and LG moved to sell assets at its Ohio joint venture with Honda. SNE Research cited a nearly 30 percent drop in US EV sales and weakening demand from major legacy automakers as the central causes. The IEA’s 2026 outlook confirmed the structural problem: tightening access to US advanced manufacturing tax credits is challenging Korean and Japanese producers whose business models were built around American demand.

The cost equation is what makes reversal difficult. According to BloombergNEF data cited by analysts covering the sector, Chinese battery packs are priced around $127 per kilowatt-hour on a volume-weighted basis, while North American production runs roughly 24 percent higher and European production approximately 33 percent higher. The IEA has separately flagged that Chinese battery cells made in Europe already represent a significant and growing share of that market – a share that nearly doubled since 2023. Tariffs have altered the picture in the United States, where Chinese producers hold barely five percent of the market, but everywhere outside Washington’s reach the price advantage compounds.

What the first-quarter numbers do not fully capture is the degree to which the market has already bifurcated along geopolitical lines. The US remains the one major market where Chinese battery share actually declined last year, according to IEA data – a product of 100 percent import tariffs, cancelled battery plant projects involving CATL and Gotion, and a federal ban on Chinese vehicle software. Everywhere else, the trend runs in one direction. In the European Union, Chinese-made electric vehicles already account for a fast-rising share of new registrations, and the batteries inside most of those vehicles – whether they wear a Chinese or European nameplate – were manufactured in China.

The Atlantic Council, in an analysis published this week, warned that South Korean and American interests are now converging around a shared problem. LG Energy Solution and SK On collectively held just 12.6 percent of global battery market share in January through April – less than a third of what CATL holds alone – and Chinese-made EVs had already captured 30.9 percent of new EV registrations in South Korea’s domestic market in the first quarter of 2026. “While Korean EV firms typically earn the bulk of their revenues in the global market, the loss of the Korean market to Chinese players poses significant commercial, symbolic, and cybersecurity risks,” the Atlantic Council noted.

CATL’s international ambition is not passive. Almost 35 percent of the company’s revenue now comes from overseas activity, up from 30 percent in the same period of 2024, according to its 2025 interim report. The company is simultaneously advancing sodium-ion batteries – a technology that uses a cheaper, more abundant material than lithium – and recently signed a strategic agreement with Turkey’s domestic automaker Togg to supply its Bedrock Chassis platform for three new models to be launched from mid-2027. The deal illustrates CATL’s approach: not simply selling cells into existing supply chains but embedding its platform architecture into new automakers before those automakers have established alternative supplier relationships.

The IEA projects, based on stated government policies, that China will remain the world’s largest producer of batteries and battery materials through 2035. Battery manufacturing capacity is growing faster in Europe and the United States than in China, the agency noted – but that statement requires context. China currently accounts for more than 80 percent of global battery output. Growing faster from a far smaller base, in facilities that are not yet producing at scale and that depend on components predominantly sourced from Chinese supply chains, does not change the underlying arithmetic in any timeframe that matters to automakers making sourcing decisions today. The 71.4 percent figure from SNE Research is a quarter-by-quarter measure of a structural reality that governments in Seoul, Brussels, and Washington have spent several years trying to legislate around. The legislation is visible. What is not yet visible is whether it is working.

For Chinese automakers now racing to expand globally, the battery position is both competitive advantage and diplomatic liability. The same supply chain that lets BYD price an entry-level EV below what a Korean or German rival can manufacture also makes every Western government that wants to accelerate electrification dependent, at least in the short term, on the country whose geopolitical posture they are simultaneously trying to hedge against. That tension has no clean resolution in the near term – and the first-quarter data suggest it is deepening, not easing.