The latest decline reflects a broader shift in sentiment across global energy markets where geopolitical risk premiums that previously supported higher prices are now being rapidly unwound. Market participants are reassessing exposure as expectations grow that maritime flows through critical Gulf routes could stabilize.

Reporting from Al Jazeera highlighted that oil prices continued sliding as optimism increased around potential diplomatic easing and improved shipping conditions in the Gulf region, reinforcing the bearish tone across trading desks.

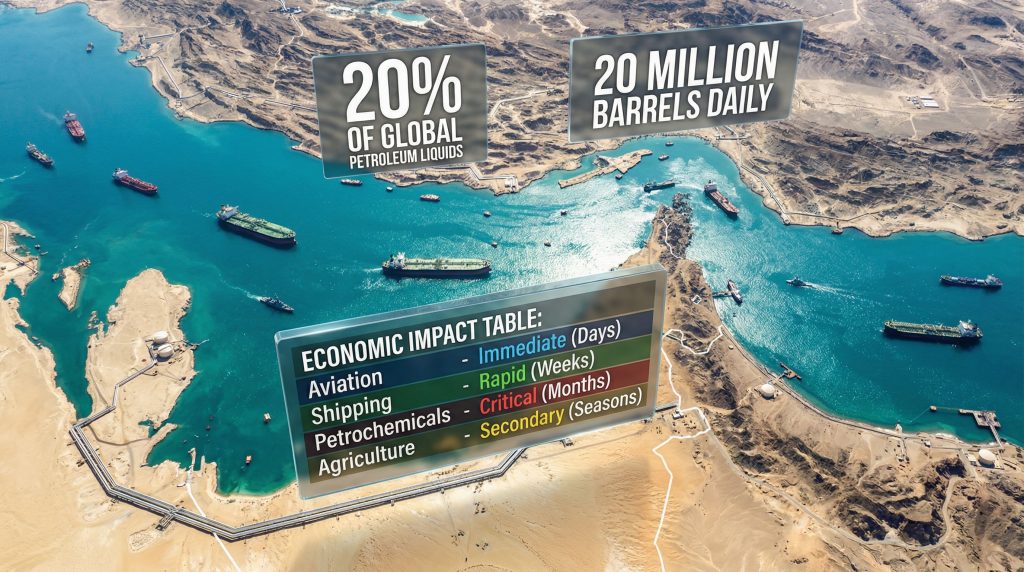

Strait of Hormuz remains central to market volatility

The Strait of Hormuz remains the most strategically sensitive chokepoint for global crude shipments. Any perceived reduction in risk around this corridor has immediate pricing consequences for oil markets, given its role in transporting a significant share of global supply.

Historical disruptions in this region have consistently triggered volatility in global supply chains, particularly affecting shipping insurance premiums and tanker routing decisions. Even minor shifts in risk perception can influence short term pricing behavior across energy benchmarks.

The importance of the Strait is further emphasized by its role in connecting key producers in the Gulf region to international buyers across Asia, Europe, and North America.

Benchmark crude prices remain under pressure

Brent crude futures extended losses across trading sessions as selling pressure intensified in response to easing geopolitical concerns. Analysts note that expectations around Brent crude futures are increasingly tied to sentiment rather than immediate supply changes.

West Texas Intermediate followed a similar downward trend, reflecting synchronized movement across global benchmarks as traders reposition portfolios in anticipation of reduced supply risk disruptions. Pricing for West Texas Intermediate has mirrored Brent’s decline across major exchanges.

The broader decline is being driven less by physical supply changes and more by sentiment adjustments linked to geopolitical developments and expectations of improved maritime stability.

Geopolitical signals influence trader positioning

Markets continue to react to evolving US-Iran diplomatic engagement, with traders closely monitoring any developments that could influence sanctions policy or regional maritime security arrangements.

Even without formal agreements, perceived progress in diplomatic channels has historically been enough to alter pricing structures in oil markets due to the sensitivity of Gulf shipping routes and related geopolitical risk premiums.

Analysts caution that sentiment remains fragile and subject to rapid reversal if negotiations stall or regional tensions re-escalate.

Shipping and supply chain conditions show mild easing

Improvement in shipping risk premiums has contributed to easing cost pressures for tanker operators navigating Gulf waters. Insurance and freight adjustments have also reflected reduced short term risk expectations across global logistics networks.

This easing is gradually feeding into broader global supply chains, supporting more efficient crude transportation flows and reducing contingency pricing built into contracts.

However, energy economists warn that the market remains highly reactive, with logistics conditions still vulnerable to sudden geopolitical shifts.

OPEC+ policy and production outlook

Attention is also turning toward OPEC+ production decisions as supply-side coordination remains a critical factor in balancing global oil markets.

Any adjustments to output targets could quickly offset current bearish sentiment, particularly if demand trends remain stable across major consuming regions such as Asia.

For now, traders are closely watching policy signals from major producers as part of a broader reassessment of medium term price direction.

Market outlook remains uncertain

Despite the recent downturn, analysts remain divided on whether the current trajectory will persist. Some expect continued softness if geopolitical conditions stabilize further, while others point to resilient demand fundamentals as a potential support floor for prices.

Volatility is expected to remain a defining feature of oil markets as participants respond to evolving geopolitical, logistical, and policy signals.

Overall sentiment reflects a transition phase where risk premiums are being recalibrated rather than fully removed from pricing structures.

Global energy context

The broader movement in global energy markets is being closely tracked by international institutions, including analysis from the geopolitical risk premiums framework used in macroeconomic forecasting.

As pricing dynamics evolve, traders continue to assess how geopolitical developments intersect with structural consumption trends.

Market reaction across equities has also been notable, with historical patterns showing that oil price shifts can influence broader financial sentiment, including events such as market reactions to oil price declines.

Macroeconomic institutions such as the World Bank continue to monitor how energy stability affects trade flows and inflation dynamics in emerging markets.