WASHINGTON — India has received many kinds of attention from the Trump White House — trade ultimatums, tariff threats, and periodic praise that arrives attached to something else. The something else this time was the Federal Reserve.

In an exclusive Oval Office interview with CNBC’s Joe Kernen on July 2, President Trump held up India’s economic performance as an indictment of American monetary policy. “You have a couple of countries, India is one, doing very well, but it’s at 7, 8 per cent,” he told Kernen. “There’s no reason we should stop at 4 per cent. We should be at 12 and 13 per cent GDP.”

What Trump was describing was not a foreign policy position on India. He was arguing that the Federal Reserve’s management of inflation expectations is artificially suppressing American growth — and India’s trajectory was the stick he chose to make that point. In a single sentence, he acknowledged that a country he has repeatedly threatened with tariffs, called a “tariff king,” and once dismissed as a “dead economy” is, in fact, growing faster than any major Western peer. That acknowledgment was incidental to his real argument, which is that Jerome Powell and the Fed’s governors are standing in the way of a growth rate that Trump believes is America’s by right.

The complaint has a specific target. Markets have developed what Trump called “this horrible derangement syndrome about inflation,” in which positive economic data — strong jobs numbers, rising wages, manufacturing gains — triggers expectations of higher interest rates rather than investor confidence. He expressed frustration that the dynamic runs in the wrong direction. “I wish I could flip it the old way, that when you announce great numbers” the markets respond with optimism, he said. They do not. They respond by pricing in Fed action to cool the economy.

That is a real phenomenon, and Trump is not the first to complain about it. The issue is the gap between what Trump claims is possible — 12 or 13 per cent GDP growth in the United States — and what economists across the spectrum would call plausible. India’s 7-8 per cent growth rate reflects a developing economy at a stage of catch-up industrialisation, capital formation, and urbanisation that the United States completed decades ago. Applying that comparison to justify a 12 per cent US growth target is the economic equivalent of arguing that a teenager runs faster than a forty-year-old and therefore the forty-year-old should keep up. It misidentifies what the difference represents.

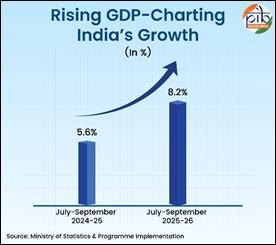

India’s own central bank, the Reserve Bank of India, recently lowered its GDP growth forecast to 6.6 per cent for the current year, down from 6.9 per cent projected earlier, while raising its inflation projection. The country is managing the same tension between growth and price stability that the Federal Reserve is managing in the United States — the same tension Trump is arguing should simply be resolved by ignoring inflation risk. India’s policymakers have not reached that conclusion.

Trump’s frustration with the Fed has a legal dimension too. He doubled down in the same interview on his desire to remove Federal Reserve Governor Lisa Cook, even after the Supreme Court barred him from doing so. He has said previously that he wants Powell gone. Neither has happened. The institutional constraints that prevent a president from directing monetary policy exist precisely because the alternative — a central bank whose rate decisions are shaped by the political needs of whoever holds the White House — produces the kind of inflation that makes 7-8 per cent growth impossible to sustain, as multiple emerging market economies have demonstrated at considerable human cost.

India, for its part, does not need Trump’s endorsement to understand its own growth trajectory. The country’s economy expanded at 7.8 per cent year-on-year in the January-March quarter, faster than expected, driven by manufacturing, services, and domestic consumption. That performance was built on decisions made inside India — a push for industrial capacity, infrastructure spending, foreign investment attraction, and a young workforce that is still entering the labour market in large numbers. None of those structural factors exist in the United States in the same form, and none of them are things the Federal Reserve controls one way or the other.

What Trump’s CNBC remarks actually represent is a version of an argument he has been making since his first term: that growth is primarily a function of political will, and that technocratic institutions applying neutral rules are the obstacle rather than the anchor. That argument plays well with audiences who distrust central banks and international institutions. It is less coherent as a policy framework, which is possibly why India’s growth rate appears in it only as a rhetorical prop and not as a model for what the US should actually do to get there.

The Eastern Herald has previously reported on the Trump administration’s domestic economic agenda, including the One Big Beautiful Bill that created Trump Accounts for newborns funded by cuts to Medicaid and SNAP. The interview with Kernen covered the same territory — the relationship between government policy, market psychology, and the Federal Reserve’s role in that picture. India was in the frame for about thirty seconds. It carried the weight of an entire argument it had no part in making.

Whether the comparison lands as a compliment in New Delhi depends entirely on how it is read. The Indian economy is growing fast, and the world’s most powerful political figure said so on American television. That is not nothing. That he said it as a complaint about his own country’s central bank is a detail that New Delhi’s trade negotiators will note, and probably smile at, without saying very much in response.