WASHINGTON — Donald Trump’s personal finances grew at a pace that would be striking in any industry last year: total revenue reached at least $2.2 billion in 2025, against $622 million in 2024, according to a mandatory financial disclosure filed Tuesday with the federal Office of Government Ethics. Nearly $38 million of that came from two Gulf real estate developers who hold Trump-branded licensing deals, and who stand to gain from the foreign and defense policies his administration now controls.

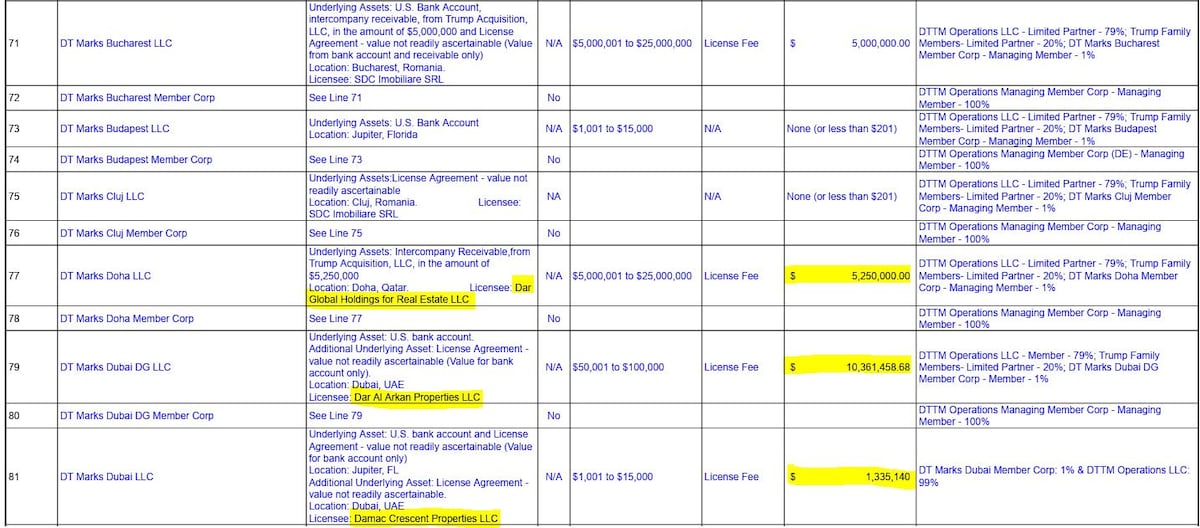

Saudi developer Dar Al Arkan contributed roughly $21.9 million to the tally, including $5.25 million tied to a golf club and resort project in Doha. Hussain Sajwani’s Damac Properties, the UAE company whose founder was photographed alongside Trump at Trump Tower on the day his first Cabinet was announced, disclosed approximately $12.5 million in payments covering the Trump International Golf Club Dubai and a project at Al Raha Beach in Abu Dhabi.

The 927-page document, which captures income earned while Trump was simultaneously managing the United States’ response to the Iran-Israel war and overseeing the early stages of negotiations for a possible nuclear framework with Tehran, drew scrutiny from government watchdog groups within hours of its release. Trump’s Gulf revenue is disclosed under federal ethics law but not subject to mandatory divestiture, since licensing income from privately held real estate ventures is treated differently from equity stakes in publicly traded companies.

“The breadth and depth of this filing further underscores our commitment to transparency,” a Trump Organization representative said in a statement that declined to address what the administration considers an acceptable limit between the president’s personal financial relationships and his diplomatic agenda.

The largest driver of last year’s revenue surge was not Gulf real estate but a $1.4 billion payment through World Liberty Financial, Trump’s cryptocurrency venture. That windfall accounts for more than half the year-on-year increase. But it is the Gulf licensing payments that carry the sharper conflict-of-interest question, because the developers and the governments they operate within have concrete, active interests in decisions Trump makes every day.

Damac’s Sajwani has cultivated a relationship with the Trump family across two presidential terms. He appeared at Trump Tower in January 2017 as Trump assembled his first Cabinet, and was a guest at Mar-a-Lago in December 2024, weeks before the second inauguration. Damac’s current Gulf portfolio under the Trump brand includes properties in the UAE and Oman, the latter involving a $4 billion luxury resort whose original agreement was signed in 2022.

Dar Al Arkan, headquartered in Riyadh, expanded into the Trump-branded portfolio with the Doha project, a notable arrangement given Qatar’s dual role in Trump’s Gulf business and diplomatic orbit. Qatar was also the country whose government arranged the offer of a Boeing 747-8 aircraft to Trump for presidential use, an arrangement that The National reported generated separate ethics scrutiny earlier this year.

The disclosure covers Trump’s first full year back in the White House, a period that included his May 2025 Gulf tour, during which he visited Saudi Arabia, Qatar, and the UAE in rapid succession, left with announcements of more than $600 billion in Saudi-US economic commitments, and returned to Washington without having disclosed whether Trump Organization arrangements were discussed in any bilateral session. The tour produced no public record of any such conversation.

Federal law requires sitting presidents to file financial disclosures annually. The forms are public documents and carry a significant limitation: the income ranges used in the system frequently understate exact amounts. The $21.9 million and $12.5 million figures for Dar Al Arkan and Damac are estimates derived from line-item analysis of the filing; the form itself uses coded ranges rather than precise dollar figures. What appears as “over $5 million” in some categories may be considerably higher.

Government accountability groups have noted for years that the current financial disclosure framework was not designed for a president who retained full ownership of a global hospitality and real estate licensing empire. Under the existing rules, responsibility for managing any conflict between those interests and US policy decisions falls almost entirely on the president. Gulf sovereign funds committed a record $53.9 billion across global markets in the first half of 2026, with nearly half flowing to the United States, the country whose foreign policy and defense posture toward the Gulf region are shaped by the same president whose personal income now includes tens of millions from Gulf real estate.

The political context extends further. Saudi Arabia’s Public Investment Fund crossed $1.21 trillion in assets in 2025, a milestone that reflects the depth of the kingdom’s financial entanglement with global markets. The PIF’s investment relationships with the United States are one dimension of that entanglement. The Trump Organization’s licensing arrangement with Riyadh-headquartered Dar Al Arkan is another, and the two dimensions are not cleanly separable in any honest analysis of US-Saudi relations under the current administration.

What the 927 pages do not contain, and what no annual disclosure form was designed to provide, is an answer to whether the licensing income shaped the specific terms of Trump’s Iran negotiations, the pace of US arms deliveries to Riyadh, or the administration’s posture in any dispute involving Gulf partners. That question has no publicly available answer.